Accounting for a non-profit organization basic version. Accounting in non-profit organizations (examples)

Accounting in non-profit organizations is carried out according to the same rules as accounting in ordinary commercial organizations. But in practice, due to the specific nature of the activities of non-profit organizations, accountants often encounter difficulties in recording certain transactions in accounting. Read more about this in our article.

Scheme of work of non-profit organizations

To understand the accounting procedures for non-profit organizations, you first need to understand the essence of their work. According to Art. 2 laws “On non-profit organizations» dated January 12, 1996 No. 7-FZ, NPOs are formed to carry out activities in public spheres:

- social;

- charitable;

- cultural and educational;

- scientific;

- sports;

- spiritual (immaterial);

- to provide legal and legal assistance to the population and organizations;

- resolution of controversial and conflict situations, etc.

Non-profit organizations can additionally engage in entrepreneurial activities, but do not have the right to distribute the profit received from it among their participants (Clause 1, Article 2 of Law 7-FZ). This means that all profits should be directed to targeted payments or organizational expenses of the NPO.

Taking into account the above, the activities of NPOs can be presented in the form of a generalized diagram:

Accounting for an NPO largely depends on whether it is engaged in entrepreneurial activities or not. Let's take a closer look at each of the options.

Accounting in non-profit organizations not engaged in entrepreneurship

If an NPO carries out only socially basic activities, then this greatly simplifies the accountant’s work, since all receipts will be credited to the account. 86, and expenses - in the debit of the account. 86.

Account The NPOs we are considering do not apply 90. A count 91 is used only when conducting transactions for the sale of assets (paragraph 2, paragraph 1, PBU 9/99, paragraph 2, paragraph 1, PBU 10/99).

Below are the entries for the main operations carried out by non-profit organizations that are not engaged in entrepreneurial activities.

|

Action |

Note |

||

|

Target funds received and included in income |

07, 08, 10, 50, 51, 52 |

VAT is not charged on target revenues (subclause 1, clause 2, article 146 of the Tax Code of the Russian Federation). If an NPO has several statutory types of activities, then 86 you need to open sub-accounts for each type. Targeted funds intended to cover administrative and organizational costs, in order to control them, also need to be transferred to a separate sub-account. 86 |

|

|

The positive (negative) exchange rate difference from the revaluation of foreign currency is reflected |

For the rules for calculating exchange rate differences, see the following articles: |

||

|

Interest on target funds placed on deposits |

This income is not taxable (subclause 43, clause 1, article 251 of the Tax Code of the Russian Federation), therefore, in the accounting of non-profit organizations, it can be immediately attributed to an increase in target funds |

||

|

Acquired fixed assets, intangible assets using targeted funds |

The VAT paid when purchasing fixed assets is included in the cost of the fixed assets and is not accepted for deduction (paragraph 2, clause 4, article 170 of the Tax Code of the Russian Federation) |

||

|

The use of target funds in the form of investments in operating systems is reflected |

|||

|

Accrual of depreciation of fixed assets |

Calculation of depreciation of fixed assets is carried out using the straight-line method once a year for the period established by the classifier depreciation groups(chart of accounts, paragraph 2, clause 17 of PBU 6/01). There is no need to calculate OS wear and tear on a monthly basis. Depreciation is not calculated for intangible assets of non-commercial organizations (clause 24 of PBU 14/2007) |

||

|

Disposal of fixed assets |

The book value of fixed assets and intangible assets was written off |

||

|

OS sales |

OS buyer payment |

||

|

When accounting for the sale of assets of non-profit organizations, they should be guided by PBU 9/99 and PBU 10/99 |

|||

|

VAT is paid only on the difference between the sale value of the fixed assets and the balance sheet (rate 20%). You can find detailed explanations in the article “Calculation and procedure for paying VAT on the sale (sale) of fixed assets” |

|||

|

Write-off of the recorded value of sold fixed assets |

|||

|

The materials remaining from the written-off (sold) OS were capitalized |

|||

|

Financial result from the sale of OS |

Profit (loss) revealed |

||

|

Profit (loss) is accounted for as undistributed |

|||

|

Retained earnings (loss) are attributed to the increase (decrease) of target funds |

|||

|

Recorded depreciation of fixed assets written off |

|||

|

Organizational costs of non-profit organizations are reflected |

Fees and other registration fees associated with organizing the activities of NPOs |

||

|

Purchase of goods and materials and assignment of their cost to implementation organizational activities NPO (input VAT is included in the cost of materials) |

|||

|

Salary and reporting expenses for employees organizing the activities of non-profit organizations |

|||

|

Rental of premises, consulting services and other organizational expenses (input VAT does not need to be allocated) |

|||

|

Property tax, land tax, transport |

|||

|

The use of targeted funds for organizational activities is reflected |

|||

|

Targeted funds are aimed at the purposes for which the NPO was created |

Funds can be transferred to both individuals and organizations |

||

|

01, 10, 50, 51, 52 |

Accounting for non-profit organizations engaged in business activities

Keeping accounting records for an NPO engaged in business is more difficult. Here, the accountant initially needs to set up strict control over the distribution of income and expenditures between socially basic activities and entrepreneurial ones.

First of all, you need to follow the wording of the purpose of the funds received and sent in contracts and primary documents. For example, the receipt of money by an NPO with the purpose of “Payment for holding a sporting event” will be regarded by tax authorities as taxable income. It would be more correct to indicate: “Targeted contribution for the organization and holding of a sporting event. VAT is not assessed." Moreover, the specified VAT mark is required.

The same goes for spending money. An accountant should avoid general statements. For example, instead of the purpose “Purchase of paper,” it is better to indicate “Purchase of paper for a charity drawing competition” or “Purchase of paper for the needs of administrative department" When maintaining accounting, such specific descriptions of the costs (payments) made will help to quickly distribute them between the correct accounting accounts.

- orders for distribution of funds;

- letters and orders of NPO participants;

- applications of citizens (organizations) to receive funds (assistance) from NPOs;

- other.

To separately account for costs for socially basic activities and entrepreneurial activities, you need to open the appropriate sub-accounts for cost accounts:

- 20-1 and 26-1 - for socially basic;

- 20-2 and 26-2 - for entrepreneurial.

The financial results of the NPOs under consideration are reflected as follows:

- from socially basic activities - on the account. 86;

- from entrepreneurship - to the account. 90, profit (loss) is written off annually to the account. 86;

- from the sale of assets (other transactions) - on the account. 91 with closing at the end of the year on the account. 86.

In the previous section, we already showed the entries compiled by non-profit organizations for socially fundamental activities and for the sale of assets. Now let’s look at the formation of transactions in an NPO for transactions related to its business:

|

Action |

Note |

||

|

Acquisition of fixed assets, intangible assets for business using targeted funds |

VAT is excluded from the cost of fixed assets and intangible assets and is deductible provided that the fixed assets and intangible assets will be used in business activities subject to VAT |

||

|

The purchase of fixed assets and intangible assets at the expense of targeted funds is reflected |

|||

|

Revenue from sales of goods and provision of services |

Accounted for under the rules applicable to commercial entities |

||

|

Costs associated with business are reflected |

Costs of remuneration of employees engaged in business |

||

|

Costs of materials, services, work third party organizations, individual entrepreneur |

|||

|

Depreciation of fixed assets, intangible assets involved in business |

|||

|

Generating business results |

Reflection in the results of the cost of purchase, production of goods sold |

||

|

Monthly attribution of incurred costs to financial results |

|||

|

Monthly closing of the account balance. 90 |

|||

|

The resulting profit (loss) at the end of the year is attributed to the increase (decrease) of target funds |

|||

|

Purchase and sale securities |

Purchase of securities. You can find detailed explanations on securities accounting in the following articles: |

||

|

Revaluation of securities (monthly or quarterly) |

|||

|

Costs of brokerage, consulting and other services related to the circulation of securities |

|||

|

Securities sold |

|||

|

The book value of securities is written off |

|||

|

Formation of results from transactions with securities |

Profit (loss) revealed |

||

|

Transfer of profit (loss) to the target funds account at the end of the year (activity) |

|||

|

With more detailed explanations of the composition financial statements You can familiarize yourself with non-profit organizations in our separate article “Accounting statements of non-profit organizations”. ResultsIt is easiest to carry out accounting for non-profit organizations that carry out only socially basic activities. The results from it are recorded on the account. 86. It is more difficult to maintain accounting for an NPO that additionally engages in entrepreneurship. In this case, the accountant will have to clearly separate the results of socially fundamental activities (with accumulation on account 86) and entrepreneurial ones (with accumulation on account 90). The results from other activities of the non-profit organization (sale of assets) are recorded in the account. 91. Profit (loss) from business and other activities must be closed at the end of the year on the account. 86. |

The article will discuss accounting in non-profit organizations. What are the features and rules, are there any nuances - further. Non-profit organizations are created for the purpose of providing charity.

Dear readers! The article talks about typical solutions legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

Despite this, they are required to maintain accounting records and pay taxes. What else do you need to know about such organizations?

Required information

Non-profit (public) organizations are created for the purpose of providing various charitable services - cultural, educational or social.

It is considered created from the moment of registration with state authorities. The life of non-profit enterprises is unlimited. Any subtype of organization must have an estimate and balance sheet.

The constituent documents are the founding agreement and the decision of the founders to create an NPO.

To register a public organization, you must provide the following documents:

- statement;

- constituent documentation (3 copies);

- decision to open an organization;

- information about the founders (2 copies);

- , confirming payment of the duty to the state

Basic terms

Division into types

The legislation allows the registration of non-profit organizations, which are divided into several types. The first is an institution (private, public and municipal).

It is created by the sole founder-owner, the purpose is to conduct non-commercial activities, managerial and cultural functions.

Such a founder can be either a citizen or a legal entity that fully or partially finances the institution. Can be converted into a fund. State and municipal are formed by the Russian Federation.

The next type is a fund. The goal is charitable, cultural and educational activities. Not subject to reorganization. Manages the fund collegial body. The activities and distribution of funds are monitored by the board of trustees.

An autonomous non-profit organization can be formed by one or more founders. Its goal is to provide services in the field of education, science, and art. This is the only type of NPO whose founders can change.

Can only be converted into a fund. A religious organization is a society of more than 10 citizens who profess a faith.

Does not have the right to transform into other organizations. The organization's property includes donations from people. Penalties are not imposed at the request of the creditor.

A public organization is an NPO, which must consist of at least 3 people. The goal is to satisfy the non-material needs of citizens. May transform into a foundation or autonomous organization.

An association (union) is created by a citizen or a legal entity, or possibly by both parties at the same time. There must be at least two founders. Can be transformed into a foundation, autonomous or public NPO.

A consumer cooperative is an NPO created to meet material needs by making contributions by members of the society.

Association of real estate owners - established by the owners of real estate for the purpose of owning, using and disposing of the property that belongs to the company.

The Chamber of Lawyers unites all lawyers of a single entity Russian Federation. Legal education is created by lawyers to carry out their activities. Formed in the form of a bureau or consultation, collegium.

Cossack Society is an NGO that unites people with the goal of preserving Cossack culture and traditions. HA Indigenous community with small in number brings together citizens from small populations to protect interests and culture.

Regulatory regulation

There are several ways to apply a simplified tax - submitting an application during registration and changing the simplified tax system.

In the first case, a special one is served. This is done upon first contact tax office when the status of a tax payer is obtained.

The second option is allowed if the NPO uses a different regime, but due to circumstances wants to switch to the simplified tax system.

There are limitations when using the simplified system:

A public organization operating under a general regime must also pay taxes. One of them is .

But, if an NPO, when receiving money for a service (for example, cultural type) acquired necessary equipment to achieve your goals, the amount will not be taxed.

Managerial

Management activities are carried out by the supreme and executive body. The main goal is control over compliance with the purpose for which the organization was created.

Management tasks:

- amendments to the constituent documents;

- determination of those activities that will be priority;

- proper use of the organization's property;

- approval of reporting;

- opening branches of NPOs;

- taking part in the activities of other public organizations.

Features of accounting

According to the law, activities are carried out on the basis. This is the main internal document that regulates the organization’s accounting procedures.

Developed and maintained by the chief accountant. The accounting policy must include the following information:

- working chart of accounts;

- forms of documents that are used to document the facts of economic activity;

- asset inventory - how it was carried out;

- what method were used to value the assets;

- how the documentation was processed;

- control over business operations;

- other issues related to accounting activities.

Tasks accounting policy NPO:

- a complete reflection of the factors of the organization’s activities;

- their timely display in reporting;

- ensure that hidden assets are not created;

- equality of indicators of analytical and synthetic accounting;

- rational accounting accounting.

Finished products

Finished goods are the final product of an organization's production process. These are the items that have been processed, meet the requirements and are put into storage.

Product accounting tasks:

- control over release and safety in the warehouse;

- correct documentation of products that were released;

- control over the implementation of the supply agreement;

- calculation of profits and costs.

Finished products are intended for sale only. To make accounting easier, a discount price is assigned, which the organization chooses independently.

As such a price, you can use your cost, price by, wholesale or retail.

Membership fees

Membership in non-profit organizations is voluntary. In accounting, contributions are designated as expenses.

If the organization receives a positive result from these expenses, then they are displayed in the reporting. Contributions are the main source of funding for public organizations.

Fixed assets

An asset is considered a fixed asset if:

- the purpose of the object is to be used in the manufacture of products;

- the object will be used for a long time - more than a year;

- the organization will not resell it;

- in future activities the object will generate income.

If the useful life of an object has expired, it is not written off, but continues to be registered with the organization and displayed in the report. Subject to write-off only when the company no longer intends to use it.

Fixed assets can come from:

- from the authorized capital;

- targeted financing;

- as a gift from other institutions or individuals;

- profit received in the course of business activities.

The basis for registering fixed assets is. Postings:

Agreements on joint activities

According to , the parties are obliged to pool contributions and act together. The condition of such an agreement is the contribution of funds for the common cause.

The number of parties can be unlimited. Non-profit organizations have the right to enter into such agreements if their purpose is not to carry out entrepreneurial activities.

There are no requirements in the legislation for the form of the agreement, so it can be drawn up both verbally and in writing. The profit received is recognized as total. It may be concluded for a specific period or indefinitely.

If one of the parties wants to leave, the other must be notified at least 3 months in advance. The grounds for termination of the contract may be:

- one of the parties is incapacitated;

- one of the comrades turned out to be bankrupt;

- death of a participant or liquidation of the company;

- personal reasons, voluntary refusal;

- the agreement has expired.

The accounting records of each party to the contract must contain information about transactions that were carried out jointly. It is necessary to highlight your share of costs and obligations, and the results of your activities.

Separate accounting of VAT in non-profit organizations

If a public organization is engaged in entrepreneurial activities, then it is a taxpayer.

Accounting in a non-profit organization must be kept on the basis of the same regulations as for commercial structures. Including, apply the Chart of Accounts approved By Order of the Ministry of Finance of Russia dated October 31, 2000 No. 94N . Recommendations for the use of existing PBUs in non-profit organizations and a list of typical postings are presented in the recommendations materials below.

Non-profit organizations, like all organizations, must submit accounting, tax, statistical reporting, reporting on insurance premiums, as well as special reporting for non-profit organizations. commercial organizations– to the territorial branch of the Russian Ministry of Justice.

Rationale

Pavel Gamolsky, President of the Association« Club of accountants and auditors non-profit organizations» How to organize accounting in a non-profit organization

Accounting in a non-profit organization (hereinafter referred to as NPO) is based on the same regulations as for commercial structures. There are only a few features.* You will learn in detail about how to apply existing PBUs in non-commercial organizations, which of them are optional, and whether it is possible to keep records in a simplified manner, you will learn from this recommendation.

PBU for non-profit organizations

Among the PBUs there are those that are optional for any non-profit organization. And there are provisions that may not apply only to certain categories of non-profit organizations.

Absolutely any NPOs may not apply in the operation of the PBUs listed in the table below.

| Name of PBUs, which are optional for all non-profit organizations | Base |

| PBU 7/98 “Events after the reporting date” | Clause 1 PBU 7/98 |

| PBU 11/2008 “Information about related parties” | |

| PBU 12/2010 “Information by segments” | Clause 1 PBU 12/2010 |

| PBU 13/2000 “Accounting state aid» | Clause 1 PBU 13/2000 |

| PBU 16/02 “Information on discontinued activities” | Clause 1 PBU 16/02 |

| PBU 17/02 “Accounting for expenses for research, development and technological work» | Clause 1 PBU 17/02 |

| PBU 20/03 “Information on participation in joint activities» | Clause 1 PBU 20/03 |

| PBU 23/2011 “Report on traffic cash» | Clause 1 PBU 23/2011 |

NGOs that do not conduct entrepreneurial activity, has the right not to apply:

- PBU 9/99 “Expenses of the organization”;

- PBU 10/99 “Income of the organization.”

But note: if an NPO sells goods (works, services, property rights) at least once and receives bank interest, then it is obliged to apply these two PBUs. This follows from paragraph 2 of paragraph 1 of PBU 9/99 and paragraph 2 of paragraph 1 of PBU 10/99.

NPOs that has the right to conduct simplified accounting , may not apply: PBU 2/2008 “Accounting for construction contracts”;

- PBU 8/2010 “Estimated liabilities, contingent liabilities and contingent assets”;

- PBU 18/02 “Accounting for income tax calculations.”

The general rules are as follows. All NPOs hand over:

Balance Sheet

NPOs fill out their balance sheets in a special way. Some sections need to be renamed. For example, Section III should be called not “Capital and Reserves”, but “Targeted Financing”. After all, NPOs do not have the goal of making a profit. Instead of capital and reserves, NPOs reflect the balance of target revenues. Balance lines that NPOs must replace in section III, are named in the table below.

| Code of the balance line whose name of the non-profit organization needs to be replaced | Line names for commercial organizations | NPO line names |

| Section III of the Balance Sheet “Capital and Reserves” | Section III of the Balance Sheet “Targeted Financing” | |

| 1310 | Authorized capital | Mutual fund |

| 1320 | Own shares purchased from shareholders | Target capital |

| 1350 | Additional capital (without revaluation) | Targeted funds |

| 1360 | Reserve capital | Fund of real estate and especially valuable movable property |

| 1370 | Retained earnings (uncovered loss) | Reserve and other target funds |

Cash flow statement

The cash flow statement of NPOs is not included in the financial statements. This is directly stated in paragraph 85 of the regulation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n.

Other reports

There are special features for funds. They are required to annually publish reports on the use of their property (clause 2 of article 7 of the Law of January 12, 1996 No. 7-FZ).

Tax reporting

All NPOs are required to submit information about the average number of employees to the tax office. This needs to be done even if there are no employees. In addition, all non-profit organizations are required to submit certificates in form 2-NDFL for each employee and calculations in form 6-NDFL.

For more information on this topic, see:

As for the rest, the composition of tax reporting in NPOs depends on the tax regime.*

Tax reporting: OSNO

Non-profit organizations submit tax reports under the general regime, which is mandatory for all organizations.

Income tax

All non-profit organizations are required to file an income tax return. This obligation does not depend on whether there is taxable income or not. This conclusion follows from paragraph 1 of Article 289 Tax Code RF.

For NPOs that do not have a profit, there are special features. They submit a declaration only once a year in a simplified format:

- Title page (sheet 01);

- Calculation of corporate income tax (sheet 02);

- Report on the intended use of property (including funds), work, services received within the framework of charitable activities, target revenues, target financing (sheet 07);

If the NPO makes a profit, the declaration must be submitted quarterly. At the same time, NPOs do not pay advance payments if sales revenues for the previous four quarters did not exceed an average of 10 million rubles. for each quarter (clause 3 of Article 286 of the Tax Code of the Russian Federation).

VAT

Non-profit organizations under the general regime are required to submit a VAT return quarterly to general procedure. If there is no object subject to VAT, hand over only front page and section 1 (clause 3 of the Procedure approved by order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/558).

An NPO can submit a single (simplified) tax return, which was approved by order of the Ministry of Finance of Russia dated July 10, 2007 No. 62n, only if it does not simultaneously have:

- object of VAT taxation;

- transactions on current accounts.

Property tax

Non-profit organizations under the general regime submit property tax returns quarterly, in accordance with the general procedure. The exception is organizations that do not have fixed assets.

Since NPOs do not charge depreciation, on lines 020–140 of Section 2 of the declaration, indicate the difference between the balance in account 01 “Fixed Assets” and the amount of depreciation in off-balance sheet account 010 (clause 1 of Article 375 of the Tax Code of the Russian Federation).

As for other tax returns, the obligation to submit them depends on whether the NPO has an object subject to the corresponding tax.

Tax reporting: simplified tax system

NPOs submit simplified reporting, which is mandatory for all organizations. In addition, simplified NPOs annually submit to the tax office a declaration on the single tax they pay (clause 1 of Article 346.12 of the Tax Code of the Russian Federation). Moreover, the obligation to submit declarations does not depend on whether there were income and expenses in the reporting period or not.

This conclusion follows from the provisions of paragraph 1 of Article 346.19 and paragraph 1 of Article 346.23 of the Tax Code of the Russian Federation.

In addition, simplified NPOs are required to keep a book of income and expenses. This is stated in the Tax Code of the Russian Federation and the Procedure, approved by order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n.

For more information on this topic, see:

- How to draw up and submit a single tax return under simplification;

Simplified NPOs do not pay income tax, property tax and VAT (Clause 2 of Article 346.11 of the Tax Code of the Russian Federation). Therefore, the NPO is not required to submit declarations for the listed taxes. But there are exceptions to this rule:

- NPOs that have property taxed at cadastral value (clause 2 of Article 346.11 of the Tax Code of the Russian Federation) pay tax on this property and submit a declaration on it in the general manner;

- NPOs are tax agents for VAT, which, for example, rent state or municipal property (clause 3 of Article 161 of the Tax Code of the Russian Federation), are required to withhold and transfer VAT and submit a declaration.

Reporting on insurance premiums

NPOs must submit reports to the Pension Fund of the Russian Federation and the Social Insurance Fund of Russia according to general rules. Those NPOs that apply reduced tariffs additionally fill out:

- in the RSV-1 form - subsection 3.3;

- in form 4-FSS - table 4.2.

Reporting to the Ministry of Justice allows you to control that NPOs do not have foreign citizens among the organization’s members, as well as foreign sources of funding.

3. From the reference book

Typical postings of a non-profit organization (NPO)

Accounting for target financing

Fixed assets: acquisition, depreciation, write-off, sale

Accounting cash transactions

Accounting for exchange rate differences

| Operation | Debit | Credit |

| Accounting for target financing | ||

| Option 1: Income is pre-accrued | ||

| The target income under the donation agreement has been accrued | 76 | 86 |

| Accrued membership fees by decision general meeting | 76 | 86 |

| 51 (50) | 76 | |

| Option 2: Income is not pre-accrued | ||

| Targeted funding has been received to the current account (cash office) | 51 (50) | 86 |

| Accounting for expenses through targeted financing | ||

| Option 1: Using accounts 20 and 26 | ||

| Salary accrued | 20-2 | 70 |

| 20-2 | 69 | |

| 20-2 | 71 | |

| 20-2 | 10 | |

| 20-2 | 68 | |

| Used target funding written off | 86 | 20-2 |

| Option 2: Using account 86 directly | ||

| Salary accrued | 86 | 70 |

| Compulsory insurance premiums charged | 86 | 69 |

| Accountable amounts included in expenses | 86 | 71 |

| Materials that were used in statutory activities were written off | 86 | 10 |

| Taxes accrued (statutory activity): land, transport, property tax, state duty | 86 | 68 |

| Fixed Asset Accounting | ||

| Acquisition of fixed assets | ||

| Fixed assets (hereinafter referred to as Fixed Assets) are purchased for business activities | ||

| Transferred to the supplier for the OS | 60-2 | 51 |

| Supplier's invoice accepted | 08 | 60-1 |

| VAT on purchased OS | 19 | 60-1 |

| Input VAT is accepted for deduction if the activity for which the object was purchased is subject to VAT | 68 | 19 |

| VAT is included in the cost of fixed assets if the activity is not subject to VAT | 08 | 19 |

| Accepted for OS accounting | 01 | 08 |

| Advance issued is credited | 60-1 | 60-2 |

| The fixed assets were acquired using targeted proceeds for statutory activities | ||

| Transferred to the supplier for the OS | 60-2 | 51 |

| Supplier's invoice accepted | 08 | 60-1 |

| VAT on the purchased object | 19 | 60-1 |

| VAT is included in the cost of the object | 08 | 19 |

| Accepted for OS accounting | 01 | 08 |

| Advance issued is credited | 60-1 | 60-2 |

| Source of funding reflected | ||

| – option 1 | 20-2 (86) | 83-4 |

| – option 2 | 86 | 86-9 |

| Depreciation of fixed assets | ||

| Accrued OS wear and tear | 010 | |

| Write-off of fixed assets | ||

| Option 1: OS was acquired using income from business activities and used in such activities | ||

| 01-B | 01 | |

| 02 | 01-B | |

| 91-2 | 01-B | |

| 10 | 91-1 | |

| Result of disposal | 99 | 91-9 |

| The original (replacement) cost of the asset has been written off | 83 | 01 |

| Parts that remain from dismantling | 10 | 91-1 |

| Accrued depreciation written off | 010 | |

| Option 3: fixed assets were purchased using targeted proceeds before 01/01/2000 and depreciation was calculated on them | ||

| The original (replacement) cost of the asset has been written off | 01-B | 01 |

| Accrued depreciation written off | 02 | 01-B |

| The residual value of the fixed assets has been written off | 86 | 01-B |

| Parts that remain from dismantling | 10 | 91-1 |

| Sale of fixed assets | ||

| Option 1: OS was acquired from business income and used in such activities | ||

| 76 | 91-1 | |

| VAT charged | 91-3 | 68-3 |

| The original (replacement) cost of the asset has been written off | 01-v | 01 |

| Accrued depreciation written off | 02 | 01-v |

| The residual value of the fixed assets has been written off | 91-2 | 01-v |

| Parts that remain from dismantling | 10 | 91-1 |

| Result of disposal | 99 | 91-9 |

| Option 2: fixed assets were acquired using targeted proceeds after 01/01/2000 and used in statutory activities | ||

| Buyer's debt accrued | 76 | 91-1 |

| VAT charged | 91-3 | 68-3 |

| The original cost of the OS has been written off | 83 | 01 |

| Parts that remain from dismantling | 10 | 91-1 |

| Result of disposal | 91-9 | 99 |

| Accrued depreciation written off | 010 | |

| Accounting for cash transactions | ||

| Receiving cash from the bank | 50 | 51 |

| Delivered cash to the bank | 51 | 50 |

| Salary issued from the cash register | 70 | 50 |

| Financial assistance provided | 76 | 50 |

| Issued on account (overexpenditure was reimbursed according to the approved advance report) | 71 | 50 |

| The balance of accountable amounts was returned to the cashier | 50 | 71 |

| Accounting for income from business activities | ||

| Revenue from sales is reflected | 62 | 90-1 |

| VAT charged | 90-3 | 68-3 |

| Costs written off | 90-2 | 20 |

| The result of the implementation is reflected | 90-9 | 99 |

| Contingent income tax expense accrued | 99 | 68-2 |

| Balance Reformation | ||

| - profit | 99 | 84 |

| – loss | 84 | 99 |

| Profit is added to target revenues | 84 | 86 |

| The loss is written off against target revenues (if income from business activities is insufficient or non-existent) | 86 | 84 |

| Accounting for exchange rate differences. Receipt and sale of target funds in foreign currency | ||

| A donation has been received to a transit currency account | 52-2 | 76 |

| The donation is included in the target revenues | 76 | 86-2 |

| Foreign currency was transferred from a transit currency account to a current currency account | 52-1 | 52-2 |

| The exchange rate difference on the transit currency account is reflected: | ||

| – positive | 52-2 | 91-1 |

| – negative | 91-2 | 52-2 |

| Currency for sale listed | 57 | 52-1 |

| Funds from the sale of foreign currency are credited to the ruble account | 51 | 91-1 |

| The exchange rate difference on foreign currency in transit is reflected | 57 (91-2) | 91-1 (57) |

| The cost of sold foreign currency has been written off | 91-2 | 57 |

| Bank commission written off | ||

| – from a current account | 91-2 | 51 |

| – from a current foreign currency account | 91-2 | 52-2 |

| – withheld by the bank from funds due to the organization | 91-2 | 76 |

| 76-5 | 91-2 | |

| Result from selling currency | ||

| - profit | 91-9 | 99 |

| – loss | 99 | 91-9 |

Non-profit organizations (NPOs). It would seem, what should be taken into account? Unless it reflects the contributions of the founders and the receipt of targeted funding. However, this is only the beginning of the activities of NGOs. Features of accounting and reporting will depend on the form of the non-profit organization: bar association, charitable foundation, homeowners association, institution or society of hunters and fishermen.

Commercial organizations are legal entities whose main purpose is to make a profit. However, legal entities can be created for other purposes. Organizations for which making profit is not a priority are recognized as non-profit.

Non-profit organizations can be created in the form consumer cooperatives, public or religious organizations (associations), institutions, charitable and other foundations, as well as in other forms provided by law.

The specifics of the forms of non-profit organizations are established in Chapter 4 of the Civil Code.

A consumer cooperative is a voluntary association of citizens and legal entities on the basis of membership in order to satisfy the material and other needs of the participants, carried out through the pooling of property shares by its members.

Public and religious organizations(associations) are recognized as voluntary associations of citizens based on the commonality of their interests to satisfy spiritual or other non-material needs.

A foundation is a non-profit organization established by citizens and (or) legal entities based on voluntary property contributions, pursuing social, charitable, cultural, educational or other socially beneficial goals.

An institution is a non-profit organization created by the owner to carry out managerial, socio-cultural or other functions of a non-commercial nature.

An institution can be created by a citizen or a legal entity (private institution) or, respectively, by the Russian Federation, a subject of the Russian Federation, municipal entity(state or municipal institution).

NPO. Accounting and reporting

NPOs maintain accounting records and submit financial statements in the manner established by the legislation of the Russian Federation.

The financial statements of NPOs must contain information about their statutory and business activities.

NPOs independently develop and accept accounting reporting forms based on the samples recommended by the Russian Ministry of Finance.

In the absence of business activity and relevant data public organizations(associations) may not present as part of their financial statements:

- statement of changes in capital (form No. 3);

- cash flow statement (form No. 4);

- Appendix to the balance sheet (form No. 5);

- explanatory note.

Information on the use of budget funds is provided by NPOs receiving budget funds. The specified information is presented as part of the financial statements according to the forms established by the Ministry of Finance of Russia.

Attached to the financial statements cover letter, containing information on the composition of the financial statements presented.

Target income for NPOs

From January 1, 2011, the list of income not taken into account by non-profit organizations for profit tax purposes has been expanded.

The corresponding amendments were made by Federal Law No. 235-FZ of July 18, 2011 “On amendments to part two of the Tax Code of the Russian Federation in terms of improving the taxation of non-profit organizations and charitable activities.”

The following are not taken into account when determining the tax base for income tax:

- targeted revenues for the maintenance of non-profit organizations and the conduct of statutory activities,

- grants for the implementation of programs in the field of science, physical culture and sports (except for professional sports);

- founding and membership fees made in accordance with the legislation of the Russian Federation on non-profit organizations;

- income received free of charge by non-profit organizations in the form of work (services) performed (rendered) on the basis of relevant contracts (subclause 1, clause 2, article 251 of the Tax Code of the Russian Federation);

- property rights transferred to non-profit organizations by will in the order of inheritance (subclause 2, clause 2, article 251 of the Tax Code of the Russian Federation, previously only property was exempt);

- property rights received for the implementation of charitable activities (subclause 4, clause 2, article 251 of the Tax Code of the Russian Federation, previously only property was exempt);

- funds received by non-profit organizations free of charge for the conduct of statutory activities not related to business, from the transferred structural divisions(departments) from targeted revenues (subclause 10.1, clause 2, article 251 of the Tax Code of the Russian Federation);

- funds received by structural units (departments) from the non-profit organizations that created them, transferred from targeted revenues for the maintenance and conduct of statutory activities (subclause 10.1, clause 2, article 251 of the Tax Code of the Russian Federation).

This is important

Non-profit organizations can also carry out entrepreneurial activities if this corresponds to the purposes for which they were created.

Accounting for charitable organizations

Charitable organizations carry out their activities in accordance with Federal Law No. 135-FZ of August 11, 1995 “On Charitable Activities and Charitable Organizations” (hereinafter referred to as Law No. 135-FZ).

The sources of formation of the property of a charitable organization may be:

- founding and membership fees;

- charitable donations, grants provided by citizens and legal entities in cash or in kind;

- income from non-operating operations;

- income from activities to attract philanthropists and volunteers (organization of entertainment, cultural, sports and other public events);

- conducting campaigns to collect charitable donations;

- income from legally permitted business activities;

- income from activities business entities, established by a charitable organization;

- volunteer labor;

- other sources not prohibited by law.

The expenses of the charitable organization are carried out according to the estimate, which is integral part charity program. The charity program establishes the stages and timing of the implementation of the estimated revenues and planned expenses (expenses for logistical, organizational and other support, for remuneration of persons participating in the implementation of charitable programs, other expenses associated with the implementation of charitable programs).

The charity program is approved by the highest governing body of the charitable organization.

When implementing long-term charitable programs, the funds received are used in installed by the program deadlines.

A charitable organization has the right to use no more than 20 percent of the financial resources spent during the financial year to pay for administrative and managerial personnel. The restriction does not apply to the remuneration of persons participating in the implementation of charitable programs.

At least 80 percent of charitable cash donations are used for charitable purposes within a year of receiving the donation.

Charitable donations in kind are sent to charitable purposes within one year from the date of their receipt.

Philanthropist or charity program Other deadlines may be established.

The property of a charitable organization cannot be transferred to the founders (members) of this organization on terms more favorable than for other persons.

A charitable organization has the right to carry out business activities only to achieve its statutory goals.

Funds received by a charitable organization from carrying out other business activities are collected into the local budget and must be used for charitable purposes.

Accounting for NPOs

NPOs maintain accounting records in the generally established manner (clause 1, article 32 Federal Law dated January 12, 1996 No. 7-FZ “On Non-Profit Organizations”).

Carrying out economic activities, charities are guided by the general Chart of Accounts accounting financial- economic activity enterprises and instructions for its use.

A feature of accounting in charitable organizations is the correct reflection of targeted income, contributions, donations for the conduct of statutory activities. In this regard, we will consider the use of account 86 “Targeted financing”.

This is important

At least 80 percent of non-operating income received during the financial year, income from business entities established by a charitable organization, and income from business activities must be used to finance charitable programs.

The credit of account 86 reflects the received funds for targeted financing, and the debit reflects the write-off of funds spent in accordance with the charity program and estimate.

Targeted funds are provided to finance specific activities and cannot be used for other purposes. In this regard, charitable organizations maintain analytical records of target funds for each type of source and in the context of target programs.

The receipt of target funds in accounting is reflected by the accounting entry:

DEBIT 50 “Cash” (51 “Current account”, 52 “Currency account”) CREDIT 86 “Targeted financing”

– for the amount of received target funds. Targeted funds can be allocated to a charitable organization in kind (humanitarian aid in the form of food, warm clothing, etc.).

In this case, the receipt is reflected by the entry:

DEBIT 10 “Materials” CREDIT 86 “Targeted financing”

– in monetary terms.

Value added tax on purchased funds in this case is included in actual cost materials.

Charitable organizations need to keep separate records of inventory items received in the form of targeted funds and acquired for conducting business activities.

In case of acquisition of inventory items for carrying out business activities, their receipt is reflected by the entry:

– for the amount of acquired material assets, including VAT. In addition, charitable organizations have the right to carry out commercial activities, and, therefore, it is necessary to maintain separate analytical records of inventory items intended for use in commercial activities. It should be remembered that in such a case, the VAT presented by the supplier is separated from the cost of inventory and materials and is accounted for separately.

This is important

Non-profit organizations have the right not to apply PBU 18/02, approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n.

The acquisition of the specified inventory items is reflected by the entry:

DEBIT 10 “Materials” CREDIT 60 “Settlements with suppliers and contractors”

– for the amount of acquired material assets (excluding VAT);

DEBIT 19 “Value added tax on purchased assets” CREDIT 60 “Settlements with suppliers and contractors”

– for the amount of VAT presented by suppliers on purchased material assets. The acquisition of inventory items is formalized in accordance with the generally established procedure.

Let's consider the reflection of business transactions on specific examples.

Example 1

A charitable foundation donates a car to a large family. The car was purchased by the fund using targeted funding for the conduct of statutory activities. The fund does not conduct entrepreneurial activities.

The initial cost of the car is 354,000 rubles. (including VAT). As of the date of transfer, the depreciation of the car was 100 percent. The market value of the car (excluding VAT) is 100,000 rubles.

The transfer of goods free of charge as part of charitable activities in accordance with Law No. 135-FZ is not subject to VAT. The exception is the transfer of excisable goods (subclause 12, clause 3, article 149, subclause 6, clause 1, article 181 of the Tax Code of the Russian Federation).

A passenger car is recognized as an excisable product. And when transferring the car, VAT should be charged (paragraph 2, subparagraph 1, paragraph 1, Article 146, subparagraph 12, paragraph 3, Article 149 of the Tax Code of the Russian Federation). The tax base is recognized market value(excluding VAT) of the transferred car, calculated in the manner prescribed by Article 40 of the Tax Code (clause 2 of Article 154 of the Tax Code of the Russian Federation).

Accounting

A car used by an NPO in its statutory activities is accounted for as part of a fixed asset (fixed asset) item at its original cost (clause 4 of PBU 6/01, approved by order of the Ministry of Finance of Russia dated March 30, 2001 No. 26n).

When accepting a car for accounting, the organization reflects the use of targeted financing funds by making an entry in the debit of account 86 “Targeted financing” in correspondence with the credit of account 83 “Additional capital” (see letter of the Ministry of Finance of Russia dated July 31, 2003 No. 16-00-14/243 ).

Non-commercial organizations do not charge depreciation on fixed assets (paragraph 3, clause 17 of PBU 6/01). Off-balance sheet account 010 “Depreciation of fixed assets” reflects the amounts of depreciation accrued in a linear manner in the manner established in paragraph 19 of PBU 6/01.

The transfer of one's own property for charitable purposes can be reflected using account 91 “Other income and expenses” (paragraph 2, paragraph 1, paragraph 5, paragraph 11 of PBU 10/99, approved by order of the Ministry of Finance of Russia dated May 6, 1999 No. 33n ).

When a car is disposed of, the amount of accrued depreciation is written off from off-balance sheet account 010. The amount of additional capital formed when purchasing a car is written off from account 83 to account 84 “Retained earnings (uncovered loss)” (paragraph 4, clause 6, Features of the formation of financial statements of non-profit organizations, published on the official website of the Russian Ministry of Finance).

The amount of VAT accrued upon transfer of the car is debited to account 91, subaccount 91-2 “Other expenses”.

Corporate income tax

Target revenues received charitable foundation and used for their intended purpose, profits are not taken into account for tax purposes (paragraph 1, 3, paragraph 2, article 251 of the Tax Code of the Russian Federation). Property acquired by the fund at the expense of targeted proceeds is not subject to depreciation in tax accounting (subclause 2, clause 2, article 256 of the Tax Code of the Russian Federation).

Expenses associated with the transfer of property for charitable purposes, including the amount of accrued VAT, premises, transport, stationery and printed materials) amounted to 50,000 rubles. The action is carried out by volunteers.

Accounting

The expenses of NPOs for carrying out a targeted event are accumulated in account 20 “Main production”. When conducting a charitable event, expenses are written off to the debit of account 86 “Targeted financing” (Instructions for the use of the Chart of Accounts, approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, clause 29 Features of the formation of financial statements of non-profit organizations, published on the official website of the Ministry of Finance Russia).

for tax purposes, profits are not taken into account (clause 16 of Article 270 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated February 5, 2010 No. 03-03-06/4/9).

Personal income tax (NDFL)

Amounts of one-time financial assistance paid as part of charitable assistance are not subject to personal income tax (clause 8 of article 217 of the Tax Code of the Russian Federation).

Consequently, when transferring a car to an individual, a charitable foundation does not have the duties of a tax agent (see letter of the Ministry of Finance of Russia dated April 8, 2011 No. 03-04-06/6-83).

Accounting entries

The cost of a car donated for charitable purposes has been written off:

DEBIT 91-2 CREDIT 01

– 354,000 rub.

The amount of depreciation accrued on the transferred vehicle is written off:

CREDIT 010

– 354,000 rub.

The additional capital generated when purchasing a car is written off:

DEBIT 83 CREDIT 84

– 354,000 rub.

Example 2

Reflection of a charitable event in the accounting of a charitable foundation.

The charitable foundation distributes free food packages to the poor. Target funds in the amount of 200,000 rubles were received into the current account. Products were purchased for distribution to the poor in the amount of 118,000 rubles. (including VAT). Expenses for the event (rent

Value added tax (VAT)

Goods and services were purchased by the fund to carry out transactions not subject to VAT. Consequently, the amount of input VAT presented on rent of premises, transport, stationery and printed materials is not accepted for deduction (subclause 1, clause 2, article 171 of the Tax Code of the Russian Federation). The amount of input VAT is included in the cost of purchased goods and services in the manner established by subparagraph 1 of paragraph 2 of Article 170 of the Tax Code.

Corporate income tax

Targeted income received by a charitable foundation and used for its intended purpose is not taken into account for profit tax purposes (paragraph 1, paragraph 3, paragraph 2, article 251 of the Tax Code of the Russian Federation). Consequently, the costs of holding a charitable event are not recognized as expenses for income tax purposes.

Accounting entries

The receipt of targeted funds is reflected:

DEBIT 51 CREDIT 86

– 200,000 rub.

The purchase of products using targeted funding is reflected:

DEBIT 10 CREDIT 60

– 118,000 rub.

The costs of holding a charity event are reflected:

DEBIT 20 CREDIT 10, 60, 76

– 168,000 rub. (118,000 + 50,000).

The use of targeted funding is reflected:

DEBIT 86 CREDIT 20

– 168,000 rub.

G. Jamalova, expert editor

General information by configuration

The software product is developed based on the configuration 1C: Enterprise Accounting, edition 2.0, preserving all standard mechanisms and capabilities of this configuration.

Functionality programs allow you to maintain simultaneous accounting of commercial and non-profit activities, accounting and tax accounting of all other areas of the organization - through integration with the program 1C: Enterprise Accounting.

Full integration of commercial and non-commercial activities has been implemented into the following accounting areas:

- materials accounting;

- warehouse accounting;

- accounting trading operations;

- accounting for cash transactions;

- accounting of fixed assets and intangible assets;

- production accounting;

- accrual wages;

- accounting of economic activities of several organizations in a single database.

The program allows the use of any tax regimes (STS, UTII, regular taxation system, individual entrepreneurs) and the transition from one tax regime to another in work base in a few minutes.

Mechanism for recording business transactions by sources of financing

Feature software product Rarus: Accounting for a non-profit organization is that the ability to select a source of financing has been added to all documents.

The program allows you to maintain a list of sources of funding for a non-profit organization.

Separate accounting of all business transactions by sources of financing is provided.

The program has the ability to control the expenditure of funds by funding sources. When posting a document and there is an overspend by source, the system displays a corresponding message.

The program implements a mechanism for automatically conducting business transactions using distributed (composite) sources of financing, when transactions must be divided in proportion to the composition of the source

It is possible to automatically distribute the amounts of business transactions across several sources of financing.

- Immediately upon posting the document ( when the Distribute by sources checkbox is enabled).

- At the end of the month the document Distribution of sources per month.

Targeted financing

In the program Rarus: Accounting for a non-profit organization The ability to account for various accruals/contributions has been implemented.

To account for the receipt of targeted funds, the following options are provided:

- Accounting option without accrual of income (Cash method)

- Accounting option with preliminary accrual of income.

The program allows you to issue payment notices to NPO members.

The program provides the ability to reflect transactions involving the gratuitous receipt of property.

And for the gratuitous transfer of property.

In the program Rarus: Accounting for a non-profit organization It is possible to send SMS.

It is possible to activate the module using a PIN code, as a result of which an account is automatically created. In the account settings, the user can view all the necessary information and can also set:

- The period during which sending SMS will be suspended;

- Maximum SMS length (limit on the number of SMS characters) and unwanted SMS length (when checking the sending message document, a warning about the presence of such lines will be issued).

The program has the ability to top up your balance. A special built-in module allows you to automate the process as much as possible mass mailing SMS, saving time and money.

The program allows you to view:

- "Usage Statistics" Here the user can see in a chart the number of messages sent for sending and sent to recipients.

- The user can look at the “Dynamics of balance changes”, i.e. the number of SMS on the balance and the average volume of one send.

Using the service, it is possible to send messages simultaneously:

- One user

- Multiple users. The recipients field can be filled in manually or automatically; to do this, you just need to remove the selection and refill the “Recipients” field.

It is possible to send messages at a certain period or immediately after creating a document.

The system allows you to send up to 300 messages per second to the numbers of any telecom operators.

In the Rarus: Accounting program for a non-profit organization, there are “Rules for selecting recipients”.

A list of selection comparison types is provided.

The program has the ability to create a message template for all users, send informational SMS to company employees - this can be company news, notifications about the need to quickly contact the client, messages about an incoming order, etc.

In many non-profit organizations, the question often arises: “Where will the funds come from to achieve their goals?” To resolve this issue it is necessary to involve financial resources, that is, fundraising. Using SMS messaging, you can easily and quickly deliver an advertising or informational message to your customers, regardless of their number and current location.

Cost accounting for non-commercial activities

In the program Rarus: Accounting for a non-profit organization it is possible to maintain 20 accounts Main production by subaccount: Main production, Production of products from customer-supplied raw materials and Costs of non-commercial activities.

It is possible to record expenses on the account 26 General expenses in terms of two sub-accounts: General commercial commercial And

Implemented automatic closing of subaccounts 20.3 Costs of non-commercial activities and subaccounts 26.02 General economic non-profit to the account 86 Targeted financing document Closing the month.

OS wear and tear

In the program Rarus: Accounting for a non-profit organization Features of accounting for fixed assets in non-profit organizations have been implemented.

Accounting for fixed assets and depreciation are provided.

Report implemented OS wear sheet. The report can display data on the depreciation of fixed assets accrued for the period.

Reporting

For the convenience of users, in standard accounting reports it is possible to obtain information on each of the sources of financing, or on all sources of financing at once.

There is the possibility of grouping and selection by funding sources.

In the program Rarus: Accounting for a non-profit organization implemented specialized reporting non-profit organizations.

It is possible to automatically fill out the balance sheet of a non-profit organization and a report on the intended use of funds received with the ability to decipher each line.

Implemented statistical reporting in form 1-NKO Information on the activities of a non-profit organization with the possibility of automatic completion and form TZV-NKO Information on the expenses of a non-profit organization.

Statistical reporting was implemented to the Ministry of Justice in form No. ON0001 Report on the activities of a non-profit organization and information on the personnel of its governing bodies.

Statistical reporting was implemented in the Ministry of Justice according to form No. ON0002 Report on the expenditure of funds and the use of other property, including those received from international and foreign organizations, foreign citizens and stateless persons.

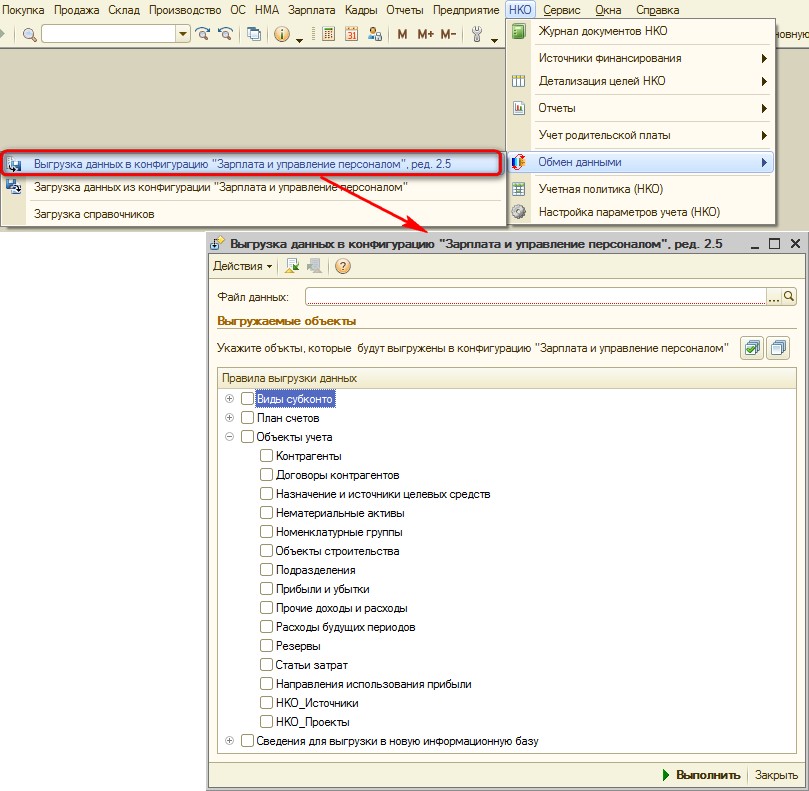

Two-way data exchange with 1C configuration: Salary and personnel management 8

In the program Rarus: Accounting for a non-profit organization The ability to exchange data with the configuration has been implemented.

It is possible to transfer to the configuration 1C: Salary and personnel management information about the chart of accounts, types of subaccounts and objects of analytical accounting (including Projects and Sources).

Accounting for parental fees

In the program Rarus: Accounting for a non-profit organization implemented additional opportunity to account for parental fees:

- the ability to store information about children (pupils of a child care institution)

- accounting of charges and payments of parents for the maintenance of children

- possibility of generating receipts

- possibility of forming an application individual to transfer funds to pay for child support

- flexible setting of parental fee rates

- the ability to generate a statement of settlements with parents for child support

- accounting for parental pay compensation with the ability to generate a compensation calculation sheet